Coinbase’s new credit fund shows why banks are fighting stablecoin yield on the Clarity Act

While Washington attempts to navigate the stablecoin battle between banks and crypto companies over the Clarity Act, Coinbase has now announced the “Coinbase Stablecoin Credit Strategy” (CUSHY), targeting qualified investors and institutions with exposure to public, private, and opportunistic credit.

The firm also said that it offers investors access to the structural alpha from tokenization, protocol incentives, and on-chain market structure.

The launch is a direct bet that stablecoins, which topped $33 trillion in transaction volume in 2025 and had an average of 89 million daily holding addresses, are mature enough to serve as distribution rails for institutional credit.

Coinbase already earns heavily from stablecoin economics, with $1.35 billion in stablecoin revenue in 2025, and subscriptions and services accounting for 41% of net revenue, against total net revenue of $6.88 billion.

Optional tokenized shares run on Superstate’s FundOS platform, with Northern Trust as the fund administrator, Coinbase Prime as the prime services provider, and Base, Solana, and Ethereum as the supported networks.

CUSHY fits Coinbase’s existing trajectory by converting stablecoin infrastructure into an asset management product with recurring institutional relationships.

ItemDetailProductCoinbase Stablecoin Credit Strategy (CUSHY)IssuerCoinbase Asset ManagementTarget investorsQualified investors and institutionsStrategy focusExposure to public, private, and opportunistic creditAdditional return sourcesStructural alpha from tokenization, protocol incentives, and on-chain market structureShare structureOptional tokenized sharesTokenization platformSuperstate FundOSFund administratorNorthern TrustPrime services providerCoinbase PrimeSupported networksBase, Solana, EthereumStrategic significanceTurns stablecoin infrastructure into an institutional credit-distribution and asset-management product rather than a pure payments or trading rail

The credit layer stablecoins haven’t touched yet

McKinsey and Artemis estimate actual stablecoin payment activity at roughly $390 billion in 2025, which is still small compared with the raw $33 trillion on-chain volume figure that Coinbase cites.

BIS similarly found annual stablecoin volumes of around $35 trillion in 2025, while acknowledging that real-economy use remained modest, with most of the raw volume reflecting trading, internal transfers, and automated activity.

Only about $8 billion of that flowed through capital markets settlement in 2025, per McKinsey.

Private credit is the most direct bridge between what stablecoins can do and what institutional finance actually needs.

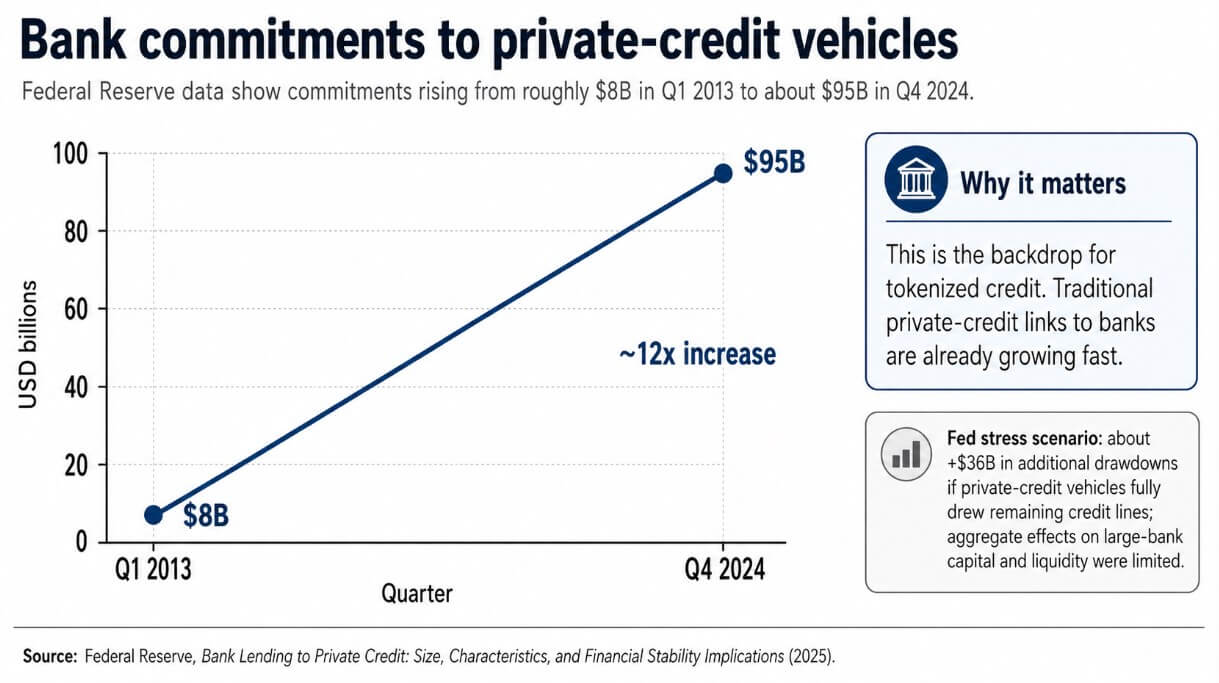

The Federal Reserve tracked bank commitments to private credit vehicles, climbing from roughly $8 billion in the first quarter of 2013 to about $95 billion in the fourth quarter of 2024.

That expansion happened entirely within traditional financial plumbing via bilateral relationships, manual fund administration, and limited secondary-market access.

In theory, on-chain rails transform subscription and transfer mechanics without affecting credit underwriting. Coinbase is betting that operational improvements alone are enough to draw institutional allocators toward tokenized structures.

BCG puts tokenized US Treasuries at $13.6 billion in April 2026, while RWA.xyz shows tokenized credit at $5.01 billion in distributed value and $21.2 billion in represented value, with represented value up 5.54% over the past 30 days.

Credit risk survives the wrapper

The technology improves subscription mechanics, transfer speed, and observability, and the underlying assets retain all the opacity, illiquidity, and borrower dependence they would in any traditional structure.

A tokenized share in a private-credit fund can move on a blockchain at any hour; no counterparty can liquidate the underlying loan on demand.

That difference between the wrapper’s apparent liquidity and the asset’s actual liquidity is the oldest risk in structured finance, and tokenization does not resolve it.

Coinbase’s CUSHY leaves the core tension between digital rail speed and credit market depth intact.

The Federal Reserve put specific numbers to private credit risk, noting a roughly $36 billion increase in drawdowns, with limited aggregate effects on large banks’ capital and liquidity ratios in a stress scenario in which private credit vehicles fully drew down their last credit lines.

The direct bank-stability implications appear contained for now, but the Fed also flagged opacity and intensifying interconnectedness between banks and private-credit vehicles as factors warranting close monitoring. Coinbase is building on a sector the Fed is watching closely.

The bull case

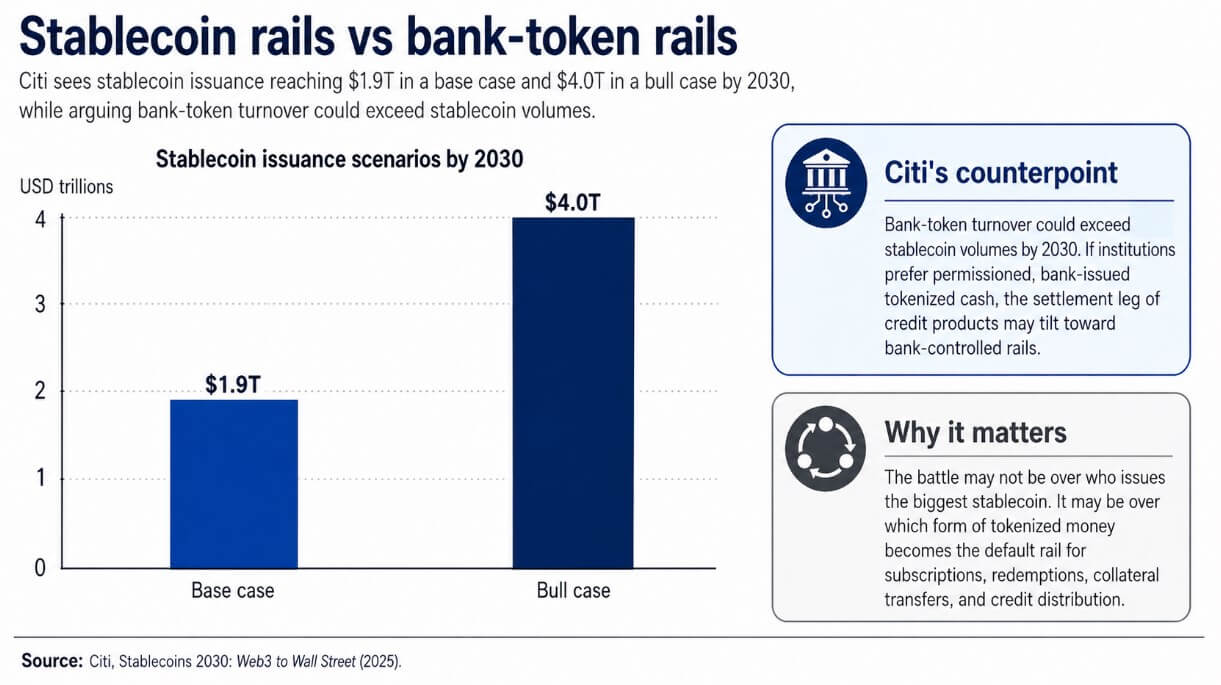

If Citi’s projection of $1.9 trillion in stablecoin issuance by 2030 in its base scenario proves directionally right, CUSHY looks early.

In that environment, stablecoins become the default money leg for fund subscriptions, redemptions, collateral movements, and secondary transfers in private-credit and asset-based-lending structures.

Coinbase’s existing infrastructure stack positions it closer to that outcome.

The $17.8 billion in average USDC balances held in Coinbase products during 2025 shows that institutional capital already sits within its infrastructure, and that pointing that capital toward credit products with recurring management economics is the natural extension.

Coinbase explicitly frames CUSHY around digitally native borrowers migrating to more efficient digital rails, a thesis backed by BIS data showing private credit lending to SaaS firms climbed from roughly $8 billion in 2015 to more than $500 billion by the end of 2025.

If those borrowers prefer on-chain access to capital, an institutional fund already running on tokenized rails and a public-chain stablecoin settlement layer gets there first.

The bear case

Citi’s analysis presents the counterargument that bank token turnover could exceed stablecoin volumes by 2030.

If institutions prefer permissioned, bank-issued tokenized cash for the settlement leg of credit products, Coinbase may help prove that institutional credit belongs on-chain while watching the most lucrative flows consolidate around bank-controlled infrastructure.

The credit thesis could be correct, and Coinbase could still find itself competing against JPMorgan’s tokenized deposit rails and similar permissioned systems for the institutional relationship.

The liquidity mismatch risk amplifies that outcome. A credit event or gating episode within a tokenized private-credit vehicle would manifest as an on-chain liquidity failure in investors’ consciousness, freezing appetite across the entire tokenized-credit category, regardless of which issuer caused it.

Coinbase’s first-mover position becomes a liability if an early stumble sets the narrative before the product matures.

The question now is whether institutional allocators trust public chain stablecoin networks more than the permissioned token systems that large banks are building in parallel.